Phone: 203-324-4680

Fax: 877-244-4578

Phone: 203-324-4680

Fax: 877-244-4578

Don't let the bank foreclose on your home. There is a more civilized, sane, less-intrusive way to get out from under your mortgage debt.

With short sales you are in control, you can get peace-of-mind and some sleep.

Don't let the bank foreclose on your home. There is a more civilized, sane, less-intrusive way to get out from under your mortgage debt.

With short sales you are in control, you can get peace-of-mind and some sleep. A short sale is when your mortgage lender(s) and/or lien-holder(s) agree to discount the loan, accepting less giving you an opportunity to sell your home at current market value. If your home is over-leveraged, underwater, or you are behind on payments and cannot sell your property for what is owed, then you may be eligible for a short sale.

A short sale is when your mortgage lender(s) and/or lien-holder(s) agree to discount the loan, accepting less giving you an opportunity to sell your home at current market value. If your home is over-leveraged, underwater, or you are behind on payments and cannot sell your property for what is owed, then you may be eligible for a short sale.

The short sale process can be a lengthy one, depending on the size of the lender it can take 2-4 months, sometimes longer, to complete. Patience and communication are the keys to its success. Lenders are inundated with short sales and are understaffed. Their procedures are often not as quick as we like them to be, but with persistence and diligent efforts we get the process done.

The short sale process can be a lengthy one, depending on the size of the lender it can take 2-4 months, sometimes longer, to complete. Patience and communication are the keys to its success. Lenders are inundated with short sales and are understaffed. Their procedures are often not as quick as we like them to be, but with persistence and diligent efforts we get the process done. The lender pays for these costs because these fees need to get paid to convey clean and clear title to the new buyer and distressed homeowners do not have the funds. It is financially advantageous for the bank to pay these costs then to have the property foreclosed upon.

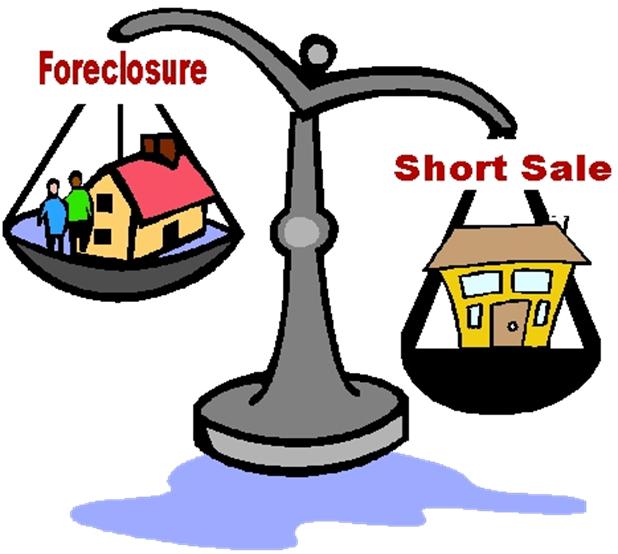

The lender pays for these costs because these fees need to get paid to convey clean and clear title to the new buyer and distressed homeowners do not have the funds. It is financially advantageous for the bank to pay these costs then to have the property foreclosed upon. The number one reason that we advocate pursuing a short sale vs. a foreclosure, is that a foreclosure will prevent you from obtaining a mortgage for a minimum of five to seven years, in addition to extensive damage to your credit, whereas a short sale will have far less impact on your credit in that most borrowers will be able to obtain a mortgage after two years of conducting a short sale. Also, the deficiency (or tax consequences) in the event of foreclosure, if is collectable, will be significantly higher than in a short sale (since properties sell at extremely discounted prices at foreclosure auctions).

The number one reason that we advocate pursuing a short sale vs. a foreclosure, is that a foreclosure will prevent you from obtaining a mortgage for a minimum of five to seven years, in addition to extensive damage to your credit, whereas a short sale will have far less impact on your credit in that most borrowers will be able to obtain a mortgage after two years of conducting a short sale. Also, the deficiency (or tax consequences) in the event of foreclosure, if is collectable, will be significantly higher than in a short sale (since properties sell at extremely discounted prices at foreclosure auctions).

CT Property Network keeps up with all the banks' ruling and changes. We are experienced in negotiating all types of liens; mortgage, IRS, construction, credit card, homeowners' associations, etc.. We will help negotiate a reasonable payoff amount, allowing you to sell your home without bringing money to the closing. Our service is absolutely free to the homeowner resulting in a clean slate for you and your family. Stop foreclosure today! Fill out our Short Sale Form and someone from our team will contact you to help you make the best decision.

CT Property Network keeps up with all the banks' ruling and changes. We are experienced in negotiating all types of liens; mortgage, IRS, construction, credit card, homeowners' associations, etc.. We will help negotiate a reasonable payoff amount, allowing you to sell your home without bringing money to the closing. Our service is absolutely free to the homeowner resulting in a clean slate for you and your family. Stop foreclosure today! Fill out our Short Sale Form and someone from our team will contact you to help you make the best decision.